A lot of people still seem anchored to the same view: recession is around the corner, markets are fragile, and every rally is just another trap. That could still happen later on, but markets often move before consensus is emotionally ready for it.

What we may be seeing now is more specific: capital gradually moving down the risk curve.

Not in one clean straight line, and not in a way that feels obvious day to day, but in the usual sequence that tends to happen when fear starts fading and liquidity conditions improve.

1. Capital usually rotates in stages

When uncertainty is high, money tends to hide in the safer or more defensive areas first.

Cash. Bonds. Gold. Mega-cap quality. Low beta names.

Only later, once confidence builds, does it start reaching for more risk:

- broad equities

- growth

- cyclicals

- small caps

- crypto

- higher beta speculation

This does not mean every cycle is identical. It means human behavior often repeats recognizable patterns.

2. Gold may have already front-run the move

Gold had a strong run while recession fears, geopolitical stress, and policy uncertainty were elevated.

That made sense.

But once an asset has already priced in a lot of fear and safety demand, it often becomes harder for fresh capital to keep pushing it vertically higher unless a new catalyst appears.

Looking at the last 18 months in historical context, the move resembles several prior runs that ended in a local top followed by a multi-month, and sometimes year-long, consolidation range.

This can mark the start of a digestion phase while money starts looking elsewhere. That does not make Gold bearish. It may simply mean the easier move already happened first, and that Gold has already caught up to much of the liquidity expansion.

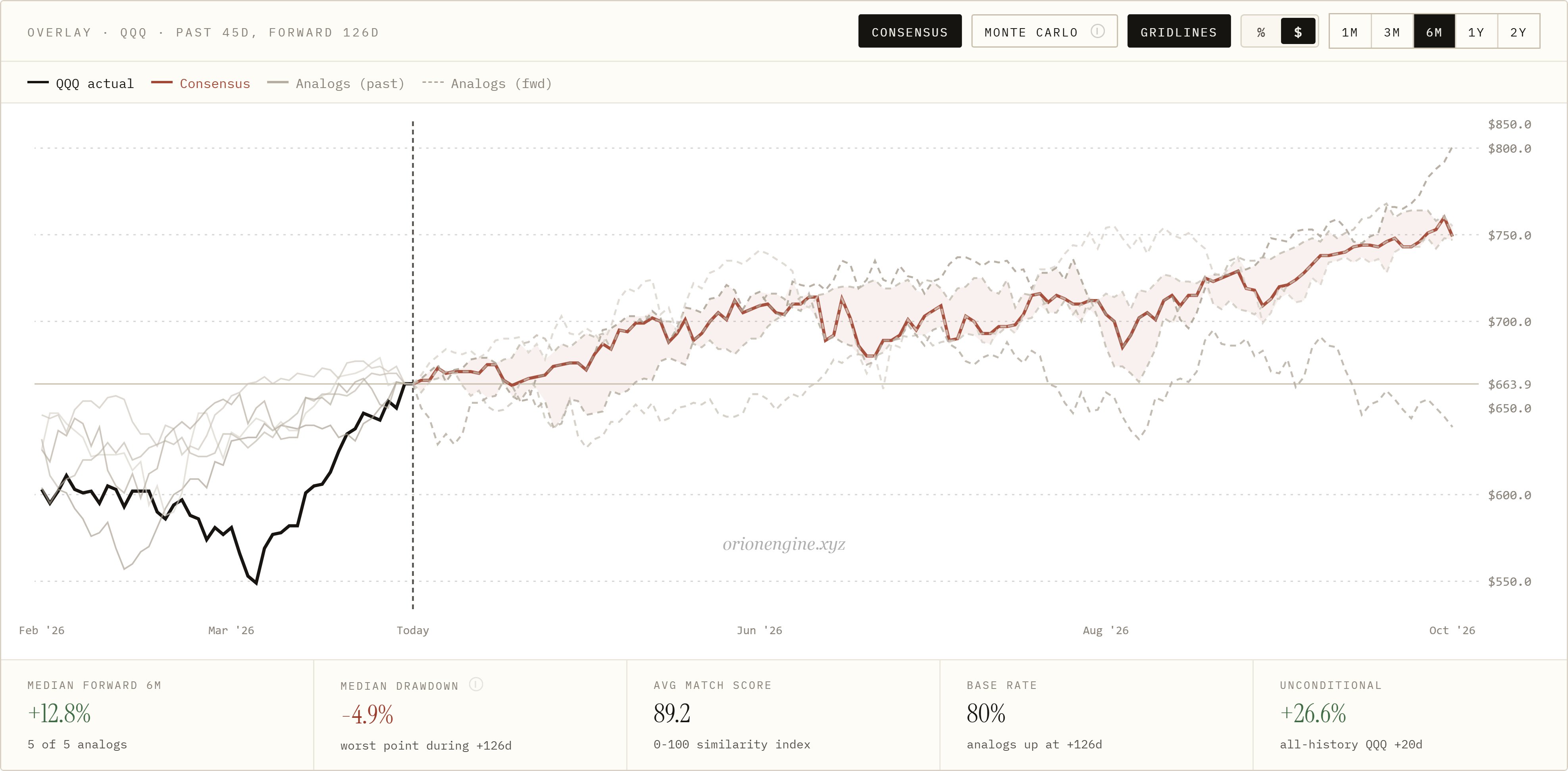

3. Equities are acting stronger than most expected

Despite constant calls for collapse, indices have remained resilient and in several areas continue grinding higher. After the recent sell-off tied to the Iran conflict, indices recovered months of downside in just a few weeks, forming a sharp V-shaped reversal.

That matters.

Markets that are truly about to break usually show broader weakness, failed bounces, deteriorating participation, and an inability to reclaim key levels. Instead, what we have often seen is persistent demand on dips.

To me, this looks less like panic and more like rotation. The closest analog overlays suggest that QQQ may simply keep grinding higher from here, which would be consistent with fresh liquidity entering the system.

4. Crypto is often later in the sequence

Crypto tends to be one of the final destinations when risk appetite expands.

Not always immediately, and not in a straight line, but historically it often benefits once:

- liquidity improves

- equities stabilize

- investors regain confidence

- appetite for higher volatility returns

That is why periods of frustration and boredom in crypto can sometimes happen right before conditions improve.

Many participants sell the range after enduring it, only to want back in once price is already higher.

That pattern is older than crypto itself.

What is interesting is that over the same one-year window we used for Gold, BTC is showing the opposite profile: a setup that suggests the low may already be in, with the next expansion phase potentially ahead.

5. Why many are still positioned the other way

Because emotionally, the bearish case still feels cleaner.

There are real concerns:

- slowing growth

- valuations

- debt levels

- geopolitics

- policy uncertainty

None of that is fake.

But markets do not reward what sounds smartest. They respond to positioning, liquidity, expectations, and whether bad news is already known.

If too many people are waiting for the obvious recession trade, markets often take a more inconvenient path first.

For those allocating capital, recognizing whether an asset may have already seen its expansion phase, like Gold, or may still be ahead of it, like Crypto, can help navigate these rotations more effectively.

6. What would invalidate this view

No framework should be treated as gospel.

I would become far more cautious if we started seeing:

- sustained credit stress

- failed index breakouts

- broad leadership deterioration

- Gold re-accelerating while risk assets roll over

- BTC losing relative strength after repeated failed recoveries

That would suggest rotation is weaker than it appears.

7. Final thought

I am not arguing for blind bullishness.

I am arguing that capital may already be moving in a familiar order, and many are focused on the headlines while missing the flow underneath.

Gold first. Equities next. Higher beta later, if the sequence continues.

That has happened before.

The goal is not to map every candle in advance. It is to recognize where we may be in the cycle before the narrative catches up.

That is exactly the kind of problem I built ORION for: using historical analogs to help frame where we are, what has happened in similar conditions, and what paths are most plausible from here.